The Iconography phase II, in the altar area is now complete. We thank all the individuals and families who donated towards this project. Our church needs your support and even though a family can not donate funds for an entire icon, you can donate a lesser amount into the general iconography fund. We have now selected a plan for the iconography Phase III, which is the dome area of our church. Donations and pledges are accepted for this phase and you may contact father Elias or the Community office to select an icon that you would like to donate, or to simply contribute to the iconography fund in general. We truly have a magnificent church, please support it, it is for you, your children, and your grand children and for the future generations to come.

We bring to your attention another method for your donations which is not widely used

Donating shares of a public company to a charity

This condensed article is contributed by Bill Giannoulis, BAFM, CPA, CA, MAcc |Tax Services| Ernst & Young LLP| [email protected]

Many have not considered the option of donating publicly traded securities to a charity. This is a very tax-effective and smart alternative to traditional methods of donating cash. Structuring your charitable donations in a tax-effective manner can provide you AND your charity considerable benefits.

The Rules

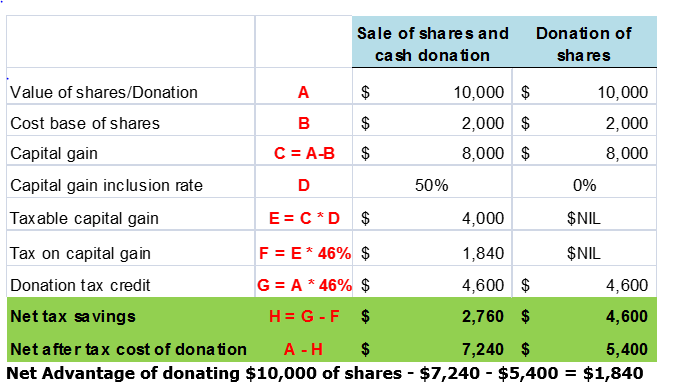

Traditionally, the disposition of shares will result in a capital gain whereby the fair market value of the shares at the time of disposition is in excess of its original purchase price. There are, however, exceptions to this rule where eligible capital property is donated to a registered Canadian charity. By definition, eligible capital property includes securities, such as shares listed on prescribed stock exchanges, as well as mutual fund units. The tax impact of donations of eligible capital property result in the capital gain reduced to nil so that the disposition of the security to the charity is fully exempt from capital gains tax.

Things to consider

In order to receive this favorable treatment, it is imperative that the security be donated directly the charitable organization. For example, selling the security in the open market and donating the cash would not qualify for this preferred tax treatment as it will result in a capital gain on disposition. By donating the shares directly to the charitable organization, the charity still receives the full benefit of the value of the share and at the same time, the donor pays no tax on the disposition and receives a charitable receipt for the fair market value of the share. This can result in significant tax benefits for those with charitable intent.

Example

For 2013, the federal credit is 15% on the first $200 of donations claimed in the year and 29% on the amount in excess of $200. The example illustrated below assumes the donor is taxed at a top marginal tax rate of 46%.

Processing the donation

Making your donation is very simple. Once you have made the decision to make your gift we can accept investment certificates and can also assist you in the transfer of securities from your current investment account. With the help of BMO Nesbitt Burns, one of Canada’s largest full-service investment firms, we are committed to making the process seamless. Contact us and we will direct you to a qualified professional who will assist you in facilitating your donation.

{kind=link}